iFIT Health & Fitness Stock: IFIT Readies $600 Million IPO

Table of Contents

nd3000/iStock via Getty Images

Quick Take

iFIT Health & Fitness (IFIT) has filed to raise $600 million from the sale of its Class A common stock in an IPO, according to an amended registration statement.

The company provides fitness equipment and related content via various revenue models including subscriptions.

While IFIT has produced impressive revenue and gross profit growth, its operating losses are a concern.

However, the firm appears well positioned for future growth potential and the IPO looks to be reasonably valued, so is worth a close look.

Company & Technology

Logan, Utah-based iFIT was founded to develop a fitness equipment and connected subscription-based exercise equipment and services company via various brands.

Management is headed by co-founder and CEO Scott Waterson, who has been with the firm since inception and was previously co-founder of iFIT’s predecessor company, Weslo.

Below is a brief overview video of the NordicTrack iFIT mobile app:

(Source)

The company’s primary offerings include:

-

NordicTrack

-

ProForm

-

iFIT Subscriptions

-

Weider

-

Freemotion

iFIT has received at least $223 million in equity investment from investors including Pamplona, L. Catterton and others.

Customer Acquisition

The firm pursues customer relationships through a direct-to-consumer [DTC] channel, large retailer channel and a commercial channel.

IFT counted 6.1 million total members of which 1.5 million were Total Fitness Subscribers for its variety of equipment including:

-

Treadmills

-

Bikes

-

Ellipticals

-

Rowers

-

Climbers

-

Strength Equipment

-

Fitness Mirrors

-

Yoga Equipment

-

Accessories

Sales and Marketing expenses as a percentage of total revenue have risen as revenues have increased, as the figures below indicate:

|

Sales & Marketing |

Expenses vs. Revenue |

|

Period |

Percentage |

|

FYE Ended May 31, 2021 |

35.5% |

|

FYE Ended May 31, 2020 |

32.7% |

(Source)

The Sales and Marketing efficiency rate, defined as how many dollars of additional new revenue are generated by each dollar of Sales and Marketing spend, was 1.4x in the most recent reporting period.

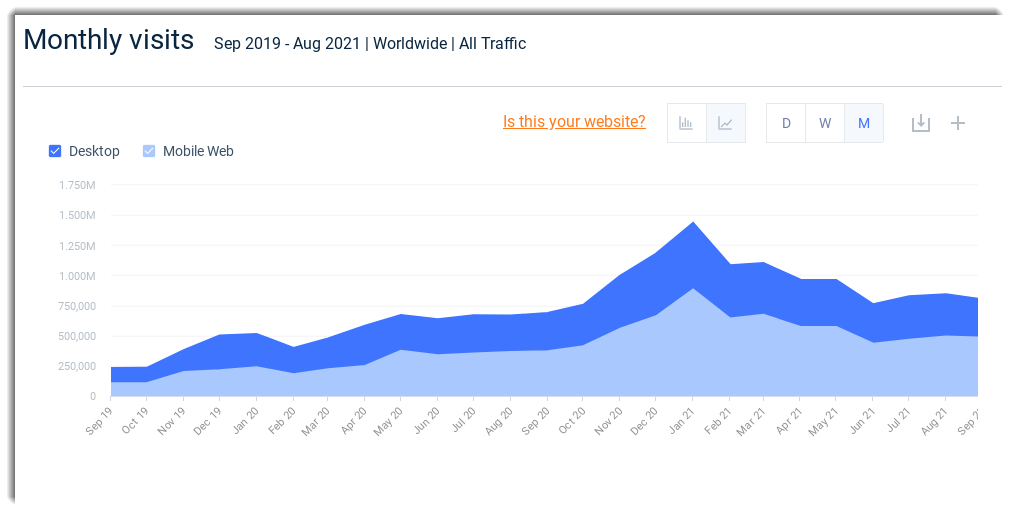

For iFIT’s subscription service, monthly visits bumped up markedly around the 2020 holiday period, generally trending higher over the past two year period, as the chart shows below:

(Source: Similarweb)

Market & Competition

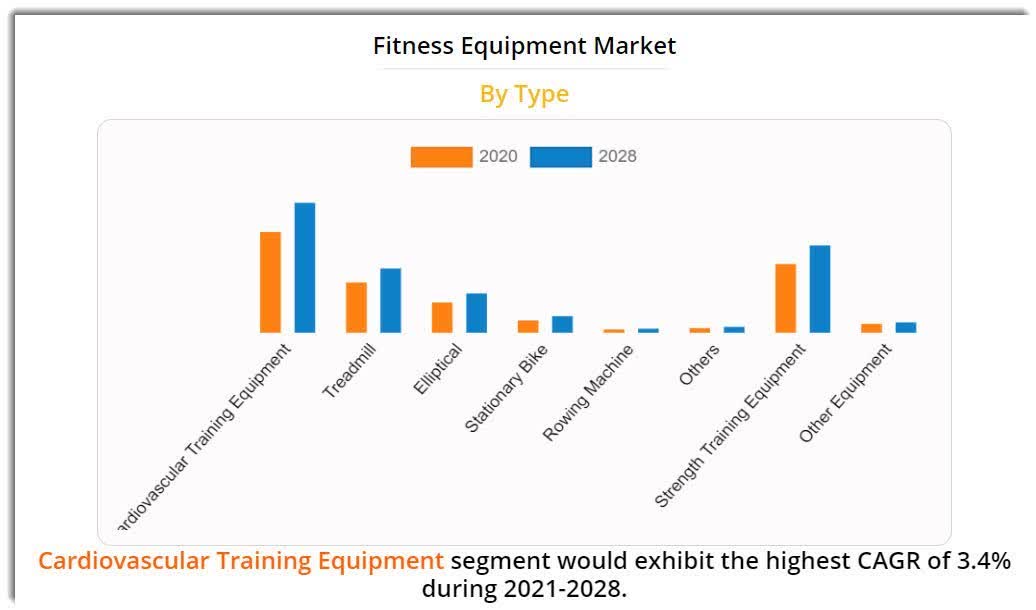

According to a 2021 market research report by Allied Market Research, the global fitness equipment market was an estimated $11.6 billion in 2020 and is forecast to reach $14.8 billion by 2028.

This represents a forecast CAGR of 3.3% from 2021 to 2028.

The main drivers for this expected growth are companies further developing technologies providing options that consumers want, such as customized workouts and display technologies along with community connections.

Also, the COVID-19 pandemic has likely brought demand forward for home-based fitness equipment and online connection as consumers spend more time at home and seek to improve their physical health in the process.

Below is a chart showing the global fitness equipment market by type as it is expected to evolve from 2020 to 2028:

(Source)

Major competitive or other industry participants include:

-

Johnson Health Tech

-

Peloton

-

Anta Sports

-

Technogym S.p.A.

-

Nautilus

-

Core Health and Fitness

-

TRUE Fitness Technology

-

Impulse Health Tech Co

-

Torque Fitness

-

Others

Financial Performance

iFIT’s recent financial results can be summarized as follows:

-

Sharply growing topline revenue

-

Strong growth in gross profit and higher gross margin

-

High operating losses and increasing negative operating margin

-

A swing to cash used in operations

Below are relevant financial results derived from the firm’s registration statement:

|

Total Revenue |

||

|

Period |

Total Revenue |

% Variance vs. Prior |

|

FYE Ended May 31, 2021 |

$ 1,745,056,000 |

104.9% |

|

FYE Ended May 31, 2020 |

$ 851,680,000 |

|

|

Gross Profit (Loss) |

||

|

Period |

Gross Profit (Loss) |

% Variance vs. Prior |

|

FYE Ended May 31, 2021 |

$ 726,203,000 |

120.8% |

|

FYE Ended May 31, 2020 |

$ 328,965,000 |

|

|

Gross Margin |

||

|

Period |

Gross Margin |

|

|

FYE Ended May 31, 2021 |

41.61% |

|

|

FYE Ended May 31, 2020 |

38.63% |

|

|

Operating Profit (Loss) |

||

|

Period |

Operating Profit (Loss) |

Operating Margin |

|

FYE Ended May 31, 2021 |

$ (127,634,000) |

-7.3% |

|

FYE Ended May 31, 2020 |

$ (49,754,000) |

-5.8% |

|

Net Income (Loss) |

||

|

Period |

Net Income (Loss) |

|

|

FYE Ended May 31, 2021 |

$ (516,706,000) |

|

|

FYE Ended May 31, 2020 |

$ (98,543,000) |

|

|

Cash Flow From Operations |

||

|

Period |

Cash Flow From Operations |

|

|

FYE Ended May 31, 2021 |

$ (13,883,000) |

|

|

FYE Ended May 31, 2020 |

$ 27,887,000 |

|

(Source)

As of May 31, 2021, iFIT had $146.5 million in cash and $1.66 billion in total liabilities.

Free cash flow during the twelve months ended May 31, 2021, was negative ($70.1 million).

IPO Details

IFIT intends to sell 30.8 million shares of Class A common stock at a proposed midpoint price of $19.50 per share for gross proceeds of approximately $600 million, not including the sale of customary underwriter options.

Class A common stockholders will be entitled to one vote per share and Class B shareholders will receive 10 votes per share.

The S&P 500 Index no longer admits firms with multiple classes of stock into its index.

No existing shareholders have indicated an interest to purchase shares at the IPO price.

Assuming a successful IPO at the midpoint of the proposed price range, the company’s enterprise value at IPO (ex- underwriter options) would approximate $5.9 billion.

Excluding effects of underwriter options and private placement shares or restricted stock, if any, the float to outstanding shares ratio will be approximately 9.77%. A figure under 10% is generally considered a ‘low float’ stock which can be subject to significant price volatility.

Per the firm’s most recent regulatory filing, it plans to use the net proceeds as follows:

approximately $465.0 million of the net proceeds will be retained by the Company and used for general corporate purposes;

$35.0 million will be used to make a required payment to our CEO; and

approximately $57.3 million ($141.7 million if the underwriters exercise their option to purchase additional shares in full) to make a cash payment, which together with the issuance of New Convertible Notes, will repay in full the 2019 Note.

(Source)

Management’s presentation of the company roadshow is available here.

Regarding outstanding legal proceedings, management says that any claims against it would be defended vigorously and would not have a material impact on its operations or financial condition.

Listed bookrunners of the IPO are Morgan Stanley, BofA Securities, Barclays and several other investment banks.

Valuation Metrics

Below is a table of the firm’s relevant capitalization and valuation metrics at IPO, excluding the effects of underwriter options:

|

Measure [TTM] |

Amount |

|

Market Capitalization at IPO |

$6,140,366,973 |

|

Enterprise Value |

$5,942,540,973 |

|

Price / Sales |

3.52 |

|

EV / Revenue |

3.41 |

|

EV / EBITDA |

-46.56 |

|

Earnings Per Share |

-$1.62 |

|

Float To Outstanding Shares Ratio |

9.77% |

|

Proposed IPO Midpoint Price per Share |

$19.50 |

|

Net Free Cash Flow |

-$70,076,000 |

|

Free Cash Flow Yield Per Share |

-1.14% |

|

Revenue Growth Rate |

104.90% |

(Source)

As a reference, a potential partial public comparable would be Peloton Interactive (PTON); shown below is a comparison of their primary valuation metrics:

|

Metric |

Peloton Interactive |

iFIT Health & Fitness |

Variance |

|

Price / Sales |

6.24 |

3.52 |

-43.6% |

|

EV / Revenue |

6.54 |

3.41 |

-47.9% |

|

EV / EBITDA |

-259.05 |

-46.56 |

-82.0% |

|

Earnings Per Share |

-$0.64 |

-$1.62 |

152.7% |

|

Revenue Growth Rate |

120.3% |

104.9% |

-12.8% |

(S-1/A and Seeking Alpha)

Commentary

iFIT is seeking to go public to make a lump sum payment to its CEO, pay down debt and for its corporate expansion plans.

The firm’s financials show very high topline revenue growth and gross profit growth, but also high operating losses and increasing negative operating margin.

Free cash flow for the twelve months ended May 31, 2021, was a hefty negative ($70.1 million).

Sales and Marketing expenses as a percentage of total revenue have risen as revenue has increased; its Sales and Marketing efficiency rate was 1.4x in the most recent reporting period.

The market opportunity for selling fitness equipment is large and expected to grow at a low rate of growth.

The firm’s subscription/membership approach has produced extremely high growth far in excess of the industry’s growth rate as it appears to grab market share and expand the addressable market for integrated workout solutions that consumers want.

Morgan Stanley is the lead underwriter and IPOs led by the firm over the last 12-month period have generated an average return of 20.6% since their IPO. This is a mid-tier performance for all major underwriters during the period.

As for valuation, compared to partial competitor Peloton, the IPO is priced considerably lower in revenue multiple terms while the firm is growing at an only slightly slower rate of growth.

While IFIT has produced impressive revenue and gross profit growth, its operating losses are a concern.

However, the firm appears well positioned for future growth potential and the IPO looks to be reasonably valued, so is worth a close look.

Expected IPO Pricing Date: October 5, 2021.